And Why Entity Selection Matters

As a small business owner, it may feel like you are your business. And often, the IRS sees it the same way. For many small businesses, whatever happens to your business’s taxes will ultimately flow down to your personal ones.

This is why tax strategy is so important. When you build a tax strategy for your business, you’re effectively building one for yourself, too.

Today, we’re sharing two more tax hacks. Unlike the first eight that we covered last week, these are a bit more complex — and they depend heavily on how your business is structured. If you want to skip ahead to the first tax hack, click here. But we first wanted to offer a primer on business structures that will make those tax hacks easier to understand.

How Small Businesses are Structured

Before we even begin, we need to clear something up from the get-go:

Legal entities and tax entities are not the same thing.

Often, your legal entity determines your tax entity — but not always.

Legal Entities

A legal entity is how your governing jurisdiction (usually your state) sees your business. It’s a legal definition — a matter of state law. While some states offer other unique types of legal entities, all recognize some version of the following:

- Corporation

- LLC (multi-member)

- LLC (single member)

- Partnership

- Sole Proprietorship

Tax Entities

Your tax entity is different: it’s how the IRS classifies your business, which determines how your income is taxed. The most common tax classifications for small businesses (and their associated tax forms) are:

- C Corporation — Form 1120

- S Corporation — Form 1120-S

- Partnership — Form 1065

- Disregarded Entity — Schedule C on Form 1040

Legal Entity ≠ Tax Entity

This is where things get interesting: your legal entity is treated a certain way by the IRS by default — but with certain elections, you can change your tax entity if you want to.

Let’s consider an entity that formed as a corporation in Delaware. By default, any incorporated entity (i.e., a corporation) will be taxed as a C corporation by the IRS (this simply means it’s governed by Subchapter C of the Internal Revenue Code). But with an election, you can change your tax entity to an S corporation (which is governed by Subchapter S of the tax code).

Let’s look at another example. Multi-member LLCs, by default, will be taxed as partnerships. But you can elect for your LLC to be taxed as a C corporation or an S corporation with the right elections. Here’s a summary of your options:

| Legal Entity | C Corporation Form 1120 |

S Corporation Form 1120-S |

Partnership Form 1065 |

Disregarded Entity Schedule C |

|---|---|---|---|---|

| Corporation | ● | ○ | ||

| Multi-Member LLC | ○ | ○ | ● | |

| Single Member LLC | ○ | ○ | ● | |

| Partnership | ● | |||

| Sole Proprietorship | ● |

● = default treatment

○ = if appropriate election is made

Keep this information in mind as we walk through the next two tax hacks. We’re going to talk about how each strategy works — and how the benefits may differ — depending on your entity type.

Hack #1: Optimizing Salary and Distributions

As a business owner, you generally get paid in two ways: (1) compensation for the work you do, and (2) distributions of business profits. Optimizing this split is our first tax hack.

C Corporation

If your entity is taxed as a C corporation, the thing you’re probably worried about most is double taxation. Corporate income is taxed once at the entity level, and when those profits are distributed to shareholders as dividends, they get taxed again. You may be able to reduce the effects of double taxation by taking a higher salary instead of distributing profits as dividends. The corporation will be able to deduct your wages as a business expense, reducing or even eliminating one level of taxation.

S Corporation

S corporations offer a valuable planning opportunity: you may be able to reduce employment taxes by paying yourself a low (yet still reasonable) salary and taking the rest as distributions. While wages are subject to payroll taxes, distributions generally are not. Just be careful: if you make your salary too low, the IRS may flag you for attempting to evade taxes.

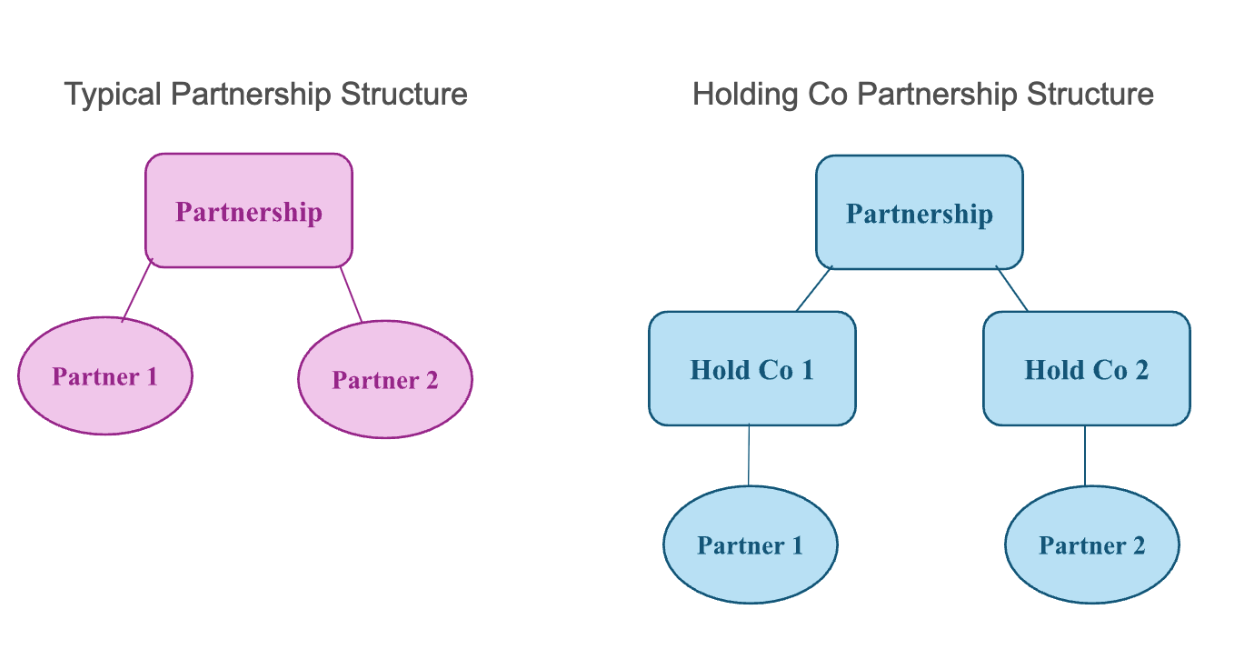

Partnership

Partnerships are a bit different. If you’re a general partner in the business, both your guaranteed payments (effectively, your “salary”) and your share of ordinary business income are generally subject to self-employment tax. Only limited partners get a break from self-employment taxes on distributions, although any guaranteed payments they receive for service would still be subject to self-employment tax. Here’s what this entity structure might look like in a 50/50 partnership:

But partnerships do have a unique opportunity that the other tax structures don’t have: By placing a holding company — typically organized as an S corporation — between the partners and the partnership, you may be able to reduce self-employment tax exposure.

When done correctly, here’s how it could work:

- The partnership continues to run the business. Instead of paying guaranteed payments or distributing income to its partners, it pays management fees or service fees to the holding companies.

- The holding companies use that money to pay W-2 wages to the partners, who are now employees of their respective holding companies.

- The partners receive wages — which are subject to payroll taxes — and may also receive distributions of profits, which are not.

This type of entity structure requires you to create new legal entities and make certain tax elections. It’s also highly scrutinized by the IRS, so you only want to proceed with this type of structure if you have a competent tax advisor to help.

But be careful…

Regardless of tax structure, your compensation/distribution split must be reasonable. We go into more detail about what “reasonable compensation” here.

Hack #2: Retirement Planning using SEP IRAs

This is another hack that requires a similar entity stacking structure that we just described — though you have to be a bit more careful to get it right.

Let’s assume you’re a partner who’s not yet 50 years old — i.e., not yet eligible for catch-up contributions. Your partnership offers a 401(k) plan. Under a traditional partnership structure, the maximum amount you and your employer can jointly put into your retirement plan (in 2026) is $72,000:

- You contribute the maximum allowed — $24,500 — via elective deferrals.

- Assuming the plan’s design and its matching/profit sharing formula allows, the partnership can contribute up to the remaining $47,500 to reach that $72,000 max.

You, as an individual taxpayer, can contribute to more than one defined contribution plan in a single year. But your combined contributions to one or more plans is $24,500 per year (in 2026).

The same is not true for employers.

The $72,000 combined employer/employee contribution maximum is available for each employer that you have. This means that if you have more than one employer, you may be able to put more away into retirement (via employer matches) than if you had only one employer.

So, how do you make that happen using an entity structure?

You may be tempted to use the same partnership + holding company structure that we described above. But this is risky. The IRS will treat multiple entities as one taxpayer under its controlled group rules if:

- There is common ownership

- One entity exists solely to support the other

- Both entities have the same owners that perform substantially the same work

- Entities have shared HR, finance, or administrative teams

That’s right: even though the partnership is a separate legal entity from the holding company, the IRS may still consider them to be the same employer for retirement plan purposes.

But there may be a way to organize your businesses in a way that achieves the desired outcome. If—

- The holding company is in an unrelated line of business

- The holding company does not primarily serve the partnership

- The holding company has additional, unrelated, third-party owners

- The holding company has a different workforce

- Each entity can stand on its own without the other—

—you may be able to use this tactic. This is where a knowledgeable tax advisor comes in handy.

But let’s assume you can create the appropriate structure — one where you are employed by both a partnership that offers a 401(k), and a holding company that offers an SEP IRA.

The same $72,000 limit applies to the partnership’s 401(k): You can contribute up to the $24,500 maximum, and your partnership can contribute up to the remaining $47,500.

But now, you’re also employed by a holding company that offers a SEP IRA. The holding company is a separate business than the partnership, which means that it has a separate $72,000 combined contribution limit. While you cannot contribute more than $24,500 between the two, you can split those contributions between both the partnership and the holding company. This might help you get more in employee matching contributions than if you only had one employer.

This is not a simple or fool-proof tax hack. It’s one that’s nuanced and requires forethought and planning when establishing your legal and tax entities. Before proceeding on this type of business structure, talk to an advisor you trust.

Still More Hacks

There are so many more tax hacks — some are simple, some more complex — that we haven’t been able to discuss. Stick around to learn more as we post them to our blog, and reach out to our team if you have further questions or if you want help implementing any of these tax strategies in your own business.