Everyone secretly hopes for an easy way to avoid overpaying taxes. Yet, many are unaware that there are ways to overcome such obligations. A perfect example of this is the Research and Development (R&D) Tax Credit, a powerful tool for easing the burden of taxation.

Did you know the research and development tax credit by the IRS helps reduce tax liability by as much as 6% to 10% federally? It is a boon for start-ups venturing into innovation, as it offers up to $500,000 in payroll tax offsets during critical growth phases. Yet many companies fail to realize its benefits.

Many companies hesitate to utilize valuable financial resources like the R&D tax credit due to complex qualification processes, unclear benefits, or a lack of awareness.

This guide aims to change that by empowering businesses with key information to leverage the benefits of R&D and confidently maximize their savings.

What is the Research and Development Tax Credit?

The R&D Tax Credit or Research & Experimentation (R&E) Credit is designed to encourage innovation and scientific advancement in the United States. It helps businesses with significant tax savings, including up to $500,000 in payroll tax offsets, and even more if they have an income tax liability.

The R&D Tax Credit was introduced as a temporary provision under the Economic Recovery Tax Act to address U.S. competitiveness. However, it later gained permanent status under the PATH Act. Today, it helps businesses save around $10 billion in taxes annually.

The credit incentivizes research and development or improvement activities by making it more profitable for businesses to invest in innovation. This helps ensure that more companies focus on R&D, driving economic growth and technological advancements.

Benefits of R&D tax credit for businesses

- Increase in cash flow.

- High tax cuts at the federal and state levels.

- Increase in market value.

- The rate of effective taxation is reduced.

- Higher profit margins.

Which Businesses are Eligible for the R&D Tax Credit?

The R&D tax credit is open to businesses of all sizes, including non-taxpayers. However, whether a company qualifies for credit depends on the money spent on the QRAs (Qualified Research Activities) outlined under IRS research and development guidelines.

Businesses that develop new products, processes, or services or enhance existing ones and incur expenses during the process could be eligible for R&D tax relief. Once claimed, the credits are offered through cash payment or a Corporation Tax reduction. To qualify for an R&D tax credit claim, businesses must invest in some form of innovation.

Manufacturing, software and technology, financial services, aerospace, e-commerce, engineering, construction, automotive, energy, and production (food and beverage, medicines) and more are some of the industries that may be eligible for R&D tax credit.

R&D Tax Credit by Industries

1) Architecture: Architects with credit amounts can invest in innovative projects such as designing energy-efficient buildings, testing new materials, or integrating modern technology into traditional design methods.

2) Engineering Firms: R&D tax credit supports innovation in new methods, materials, and processes. Engineers can benefit from tax savings while improving designs, identifying sustainable materials, or enhancing machinery.

3) Software Companies: Software firms can claim the R&D tax credit for new applications, improving user experience, or developing cutting-edge interfaces.

4) Builders and Remodelers: Builders can invest tax credits in future projects to develop new construction techniques or improve safety methods.

5) Healthcare Industry: Healthcare companies can use the R&D tax credit for new procedures, medical devices, or software. They can claim eligible expenses from the past three years, providing much-needed financial relief.

6) Food and Beverage: Businesses in this sector can benefit from testing new products, improving processes, or ensuring higher quality. The R&D tax credit acts as a fund for ongoing innovation.

7) Manufacturing: Manufacturers can remain competent and thrive by saving on taxes for activities such as creating prototypes, automating systems, or enhancing durability.

State-specific R&D Tax Credits

State-specific R&D tax credits may also exist apart from the federal R&D tax credit for businesses in the U.S., with distinct regulations and qualification criteria. Alongside federal credit, state-level credits are available, enabling companies to double rewards and savings.

However, rules for R&D tax credit regulations differ by state. For example, Southeastern states such as Florida, Georgia, Louisiana, South Carolina, and a few Midwestern states, like Minnesota, offer an R&D tax credit. On the other hand, Alabama, Mississippi, and Tennessee still do not have provisions for R&D tax credits.

With such varying tax credit availability, businesses must explore the state-specific prerequisites. Outsourcing a tax advisor or consulting a state-specific Department of Revenue offers a clear picture of current regulations and the claiming process.

Which Expenses Fall Under R&D Tax Credit?

According to the IRS in Section 41(b), R&D Tax Credit qualified expenses are those costs incurred by a company in association with research activities that meet the specific stipulations of the R&D Tax Credit. The following activities and related expenses are typically eligible:

- Engineering processes and activities related to product or technology development.

- Technology development or improving existing ones, including software.

- Development of product prototypes or patents.

- Research activities, including incomplete ones, are related to new or improved products, processes, or services.

Types of Eligible Expenses

The IRS outlines four main categories of eligible research expenses:

- W-2 taxable wages paid to employees involved in research or supporting research activities.

- Supplies used in the R&D process (not general office supplies).

- Costs related to renting computers or using cloud services for research or software development.

- Costs associated with contracted research provided the company retains substantial rights to the results and assumes the economic risk of development.

Ineligible Expenses

The R&D tax credit does not cover:

- Activities related to management functions or social sciences.

- Research conducted outside the U.S.

Note: If employees spend part of their time on a qualifying project, only a proportion of their wages will count as eligible expenses.

How Much Can You Receive from the R&D Tax Credit?

At the federal level, the R&D tax credit has no cap value and is typically worth up to 15% of qualified research expenditures. Businesses can compensate up to $500,000 of payroll taxes annually, irrespective of income generation, thus saving millions over time. Along with federal-level claims, the qualifying companies can reap the benefits of state-specific R&D tax credits and ensure more savings.

If a business does not utilize the R&D tax credit in one year, the remaining credit amount can be carried forward to future tax years. The R&D credit carryforward process can be continued for up to 20 years.

Calculating R&D Tax Credit the Right Way

Two methods can be employed to determine the R&D tax credit.

1) Regular Method: When the Credit is 20% of the company’s Qualified Research Expenditures (QREs) over a base amount. The base is calculated using a fixed-base percentage and the average gross receipts of the past four years.

2) Alternative Simplified Credit (ASC) Method: When the credit is 14% of QREs exceeding 50% of the average QREs from the past three years. If there are no previous QREs, the credit is 6% of the present year’s QREs.

Which is the Best Method?

Using R&D credit form 6765, you can calculate credits using both methods and choose the one offering the most benefit. Generally, new claimants find the ASC method simpler. For accurate calculations, however, consulting tax experts is advisable.

Claiming Process for R&D Tax Credit

Claiming for R&D tax is simple with the right approach and documentation. Here is a step-by-step claim procedure that also lists the documents to be submitted and the criteria for claiming the credit:

Step 1: Review and Assess R&D Activities

Businesses must review R&D processes during a specific tax year and plan an elaborate end of year tax strategy. This also includes identifying qualifying activities, costs, and expenses associated with those activities and their documentation.

Testing documentation of any form, such as project records, lab notes, design drawings, prototypes, and patented applications, will also fall under this. With this, accounting records, such as payroll data, expense reports, and bookkeeping records that track time and expenditures, should be documented well.

Step 2: Gathering Records and Documentation

For the IRS to accept the claim, proper documentation is essential to avoid delays or rejection of your claims. Listed are the following records to be documented.

- Tax and payroll records.

- Detailed reports on expenses and time allocation.

- Evidence linking projects to R&D efforts.

Step 3: Filing Appropriate Tax Forms

The forms businesses need depend on their revenue and age:

- Small Businesses with less than 5 years in gross receipts and under $5M in aggregate gross receipts must submit their claims through Form 6765.

- For small businesses applying the credit against payroll taxes, it is mandatory to complete Form 8974 and attach it to Form 941. This will allow them to claim up to $500,000 against employer-paid Social Security and Medicare taxes.

- Established Businesses with 5+ years in gross receipts or more than $5M in aggregate gross receipts) also need Form 6765 to claim the credit against income taxes. But here, the $500,000 limit does not apply.

Tips for claiming successfully:

- Begin Early: Start preparing documents as soon as possible to avoid last-minute glitches during tax season.

- Consult a Tax Advisor: Working with an experienced tax advisor is critical to navigating the complexities of the claim process, maximizing your benefits, and ensuring the records are well-organized and compliant.

- Avoid Filing Without Proper Records: Addressing bookkeeping gaps beforehand ensures records are complete and adequately substantiate the claim.

Documents Required

- Form 6765 to calculate and claim the credit.

- The list of qualifying activities, including R&D activities, qualified under IRS’s four-part test.

- Expense records, wage reports, supply receipts, and other proof of qualified research expenses.

- Records of time spent on R&D activities or expert-backed estimates for W-2 employees.

- Contracts for outsourced work, relevant agreements, and supporting details.

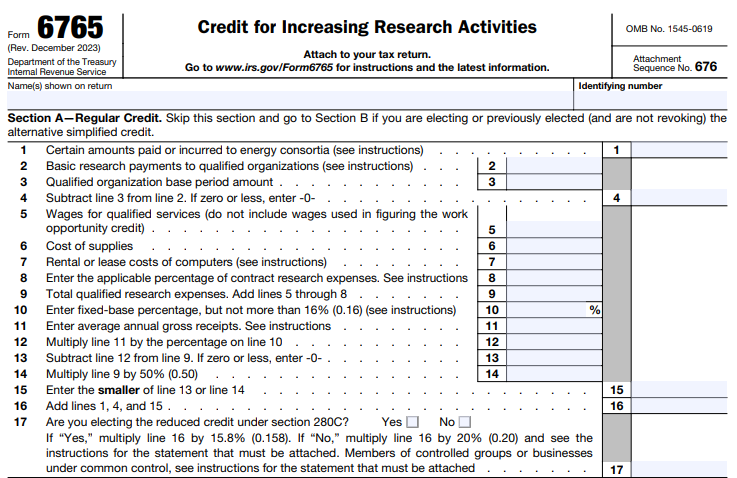

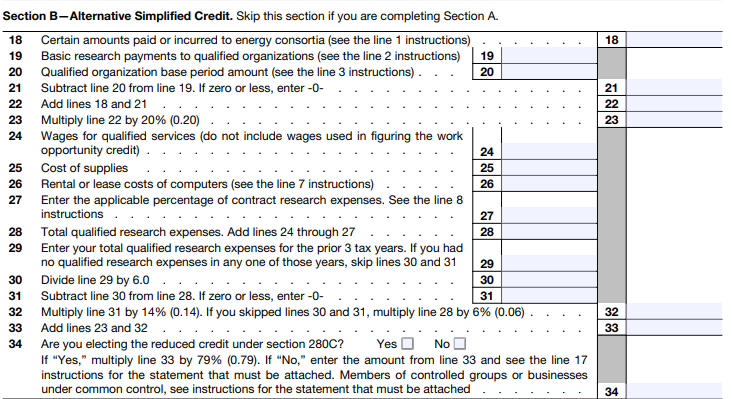

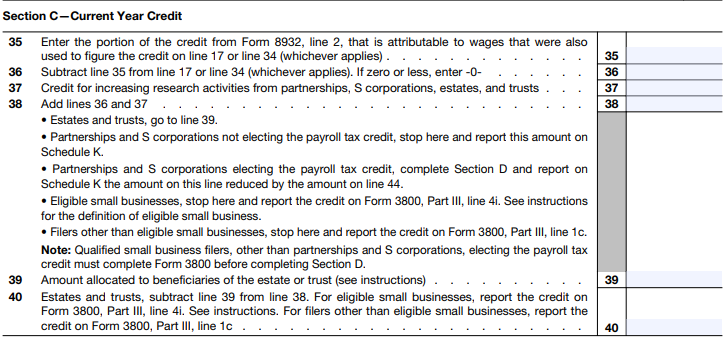

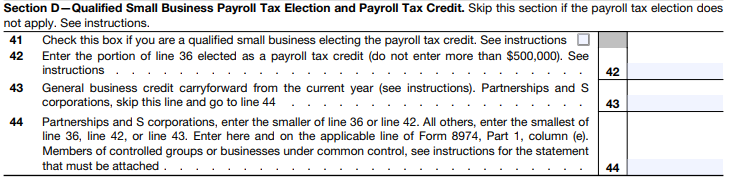

Navigating IRS Form 6765

There are four sections in Form 6765 to be filled. Here is a closer look at it.

- Sections A and B: Outlines steps for estimating tax credits. Those using the Regular Research Credit method must complete Section A. Section B is for the Alternative Simplified Credit method.

- Section C: Opens to the forms and schedules where estimated credit for the current year is reported.

- Section D: Here, qualified small businesses can apply for some or all R&D tax credits to offset payroll tax liabilities.

Prepare for the Audit

The IRS frequently audits R&D credit claims, with around 20% of claims being reviewed annually. The most common issues here are unqualified research and unsupported expenses. While an audit does not lead to penalties, being prepared is important.

To avoid issues, ensure you have clear documentation for:

- The amount and timing of each expense

- The purpose of the expense

- Its relation to your research

By building a concise case well-supported by facts, companies can improve their chances of a smooth audit process.

Summing Up the Potential of the R&D Tax Credit

For businesses investing in any kind of innovation, the R&D Tax Credit emerges as a valuable tool to reduce tax burdens, encourage innovation, and invest in growth. Since the R&D tax credit is available for every company, irrespective of size, both start-ups exploring new ideas or established businesses across industries working to improve their existing products benefit from it. At Fully Accountable, we have a team of experienced professionals who specialize in planning IRS-compliant tax strategies to reduce liabilities. With years of expertise in U.S. tax legislation and a commitment to staying current with tax changes, we empower businesses with strategic tax planning!